Bayesian Linear Regression#

A probabilistic view of a linear regression offers advantages comparing with a frequencist treatment of the linear regression model as seen in the previous labs. Let’s discuss the differences between the two approaches looking at an example with data on Kaggle. Before that, let us formally introduce some concepts and notation; I will follow your lecture’s notation and the flow of section 3.3 of Chris Bishop’s Book.

Start by considering a standard linear regression model written as

Where \(X \in \mathbb{R}^{n \times d}\) is a matrix of inputs, \(y \in \mathbb{R}^n\) is a vector of outputs, \(w \in \mathbb{R}^{d}\) a vector of parameters.

Recall from your lecture that, we have assumed for simplicity that in a Bayesian setting we have

Likelihood: \(y \sim N(Xw, \sigma^2 I) \)

Prior: \(w \sim N(0,\lambda^{-1}I)\)

For Bayesians any unknown quantity is treated as random and therefore, contrary to standard linear regression, \(w\) is vector of random variables here. This different way to think about \(w\) leads to the need of specifying its ‘Prior’ distribution that reflects our prior belief on \(w\). Here we assume a Gaussian prior for simplicity, but you can specify other types of distribution that best reflect your prior knowledge about the DGP.

Bayesian inference then proceeds by estimating the posterior which according to the Bayes Rule is proportional to the Likelihood times the Prior, i.e.

The \(\propto\) sign indicates that the quantities in both sides are proportional to each other. One important thing to notice is that, while in the standard linear regression estimation yields a point estimate of \(w\) (and respective standard deviation), Bayesians report a distribution instead (i.e. \(p(w|y,X)\)) from which one can calculate moments (eg. mean, standard deviation).

Given our choice of Prior, it turns out that in this case

with

Bayesian inference often involves Markov-Chain Monte Carlo (MCMC) algorithms such as the Gibbs Sampler or Metropolis Hastings which can be computationally expensive as model complexity grows. Variational Bayes (VB) methods are also popular as they don’t require simulation to compute posterior distributions and can therefore be faster. These alternative methods of inference are often necessary since the posterior distribution is of an unknown form.

However, in specific cases (such as the one above) where you have very simple models and conjugate priors, it may be possible to obtain a closed-form solution for the posterior distribution. Conjugate priors are chosen so that the posterior distribution belongs to the same family of distributions as the prior, simplifying the maths. These cases are the exception rather than the rule.

Maximizing the log posterior wrt. \(w\) gives the maximum-a-posterior (MAP) estimate.

In summary, while there are cases where you can obtain a closed-form solution for the posterior distribution in Bayesian linear regression, it is more common to use numerical methods like MCMC or VB to approximate the posterior distribution, especially in complex and real-world scenarios. These numerical methods provide a flexible and powerful way to estimate the Bayesian posterior when closed-form solutions are not available.

Exercise#

Think about how the previous solution compares with OLS estimators.

Now let’s see an example where we try and predict house prices in California with a Bayesian Linear Model.

# load required libraries

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

from sklearn.model_selection import train_test_split

from sklearn.datasets import fetch_california_housing

data_cali_hp = fetch_california_housing(as_frame=True)

print(data_cali_hp.DESCR) #<- uncomment to read a brief data description

data_cali_hp = data_cali_hp.frame

#data_cali_hp.info()

#data_cali_hp.head()

.. _california_housing_dataset:

California Housing dataset

--------------------------

**Data Set Characteristics:**

:Number of Instances: 20640

:Number of Attributes: 8 numeric, predictive attributes and the target

:Attribute Information:

- MedInc median income in block group

- HouseAge median house age in block group

- AveRooms average number of rooms per household

- AveBedrms average number of bedrooms per household

- Population block group population

- AveOccup average number of household members

- Latitude block group latitude

- Longitude block group longitude

:Missing Attribute Values: None

This dataset was obtained from the StatLib repository.

https://www.dcc.fc.up.pt/~ltorgo/Regression/cal_housing.html

The target variable is the median house value for California districts,

expressed in hundreds of thousands of dollars ($100,000).

This dataset was derived from the 1990 U.S. census, using one row per census

block group. A block group is the smallest geographical unit for which the U.S.

Census Bureau publishes sample data (a block group typically has a population

of 600 to 3,000 people).

A household is a group of people residing within a home. Since the average

number of rooms and bedrooms in this dataset are provided per household, these

columns may take surprisingly large values for block groups with few households

and many empty houses, such as vacation resorts.

It can be downloaded/loaded using the

:func:`sklearn.datasets.fetch_california_housing` function.

.. topic:: References

- Pace, R. Kelley and Ronald Barry, Sparse Spatial Autoregressions,

Statistics and Probability Letters, 33 (1997) 291-297

# Describe the data

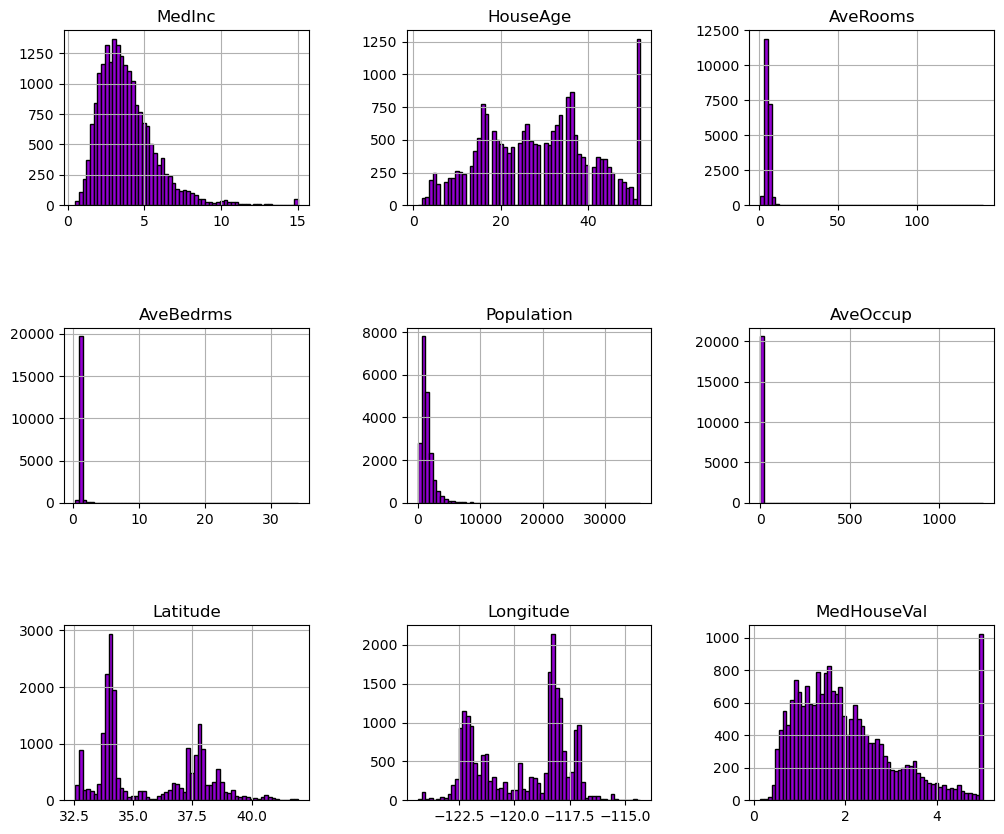

data_cali_hp.hist(bins=60, edgecolor="black", figsize=(12, 10),color='darkviolet')

plt.subplots_adjust(hspace=0.7, wspace=0.4)

plt.show()

We can first focus on features for which their distributions would be more or less expected.

The median income is a distribution with a long tail. It means that the salary of people is more or less normally distributed but there is some people getting a high salary.

Regarding the average house age, the distribution is more or less uniform.

The target distribution has a long tail as well. In addition, we have a threshold-effect for high-valued houses: all houses with a price above 5 are given the value 5.

Focusing on the average rooms, average bedrooms, average occupation, and population, the range of the data is large with unnoticeable bin for the largest values. It means that there are very high and few values (maybe they could be considered as outliers?). We can see this specificity looking at the statistics for these features:

features_of_interest = ["AveRooms", "AveBedrms", "AveOccup", "Population"]

data_cali_hp[features_of_interest].describe()

| AveRooms | AveBedrms | AveOccup | Population | |

|---|---|---|---|---|

| count | 20640.000000 | 20640.000000 | 20640.000000 | 20640.000000 |

| mean | 5.429000 | 1.096675 | 3.070655 | 1425.476744 |

| std | 2.474173 | 0.473911 | 10.386050 | 1132.462122 |

| min | 0.846154 | 0.333333 | 0.692308 | 3.000000 |

| 25% | 4.440716 | 1.006079 | 2.429741 | 787.000000 |

| 50% | 5.229129 | 1.048780 | 2.818116 | 1166.000000 |

| 75% | 6.052381 | 1.099526 | 3.282261 | 1725.000000 |

| max | 141.909091 | 34.066667 | 1243.333333 | 35682.000000 |

For each of these features, comparing the interquartile range, we can see a huge difference. It confirms the intuitions that there are a couple of extreme values.

Up to know, we discarded the longitude and latitude that carry geographical information. In short, the combination of this feature could help us to decide if there are locations associated with high-valued houses. Indeed, we could make a scatter plot where the x- and y-axis would be the latitude and longitude and the circle size and color would be linked with the house value in the district.

#! pip install geopandas geoplot

import geopandas as gpd

import geoplot as gplt

import geoplot.crs as gcrs

import mapclassify as mc

' Plot Two Geopandas Plots Side by Side '

# defining a simple plot function, input list containing features of names found in dataframe

def plotTwo(df,lst):

# load california from module, common for all plots

cali = gpd.read_file(gplt.datasets.get_path('california_congressional_districts'))

cali = cali.assign(area=cali.geometry.area)

# Create a geopandas geometry feature; input dataframe should contain .longtitude, .latitude

gdf = gpd.GeoDataFrame(df,geometry=gpd.points_from_xy(df.Longitude,df.Latitude))

proj=gcrs.AlbersEqualArea(central_latitude=37.16611, central_longitude=-119.44944) # related to view

ii=-1

fig,ax = plt.subplots(1,2,figsize=(21,6),subplot_kw={'projection': proj})

for i in lst:

ii+=1

tgdf = gdf.sort_values(by=i,ascending=True)

gplt.polyplot(cali,projection=proj,ax=ax[ii]) # the module already has california

gplt.pointplot(tgdf,ax=ax[ii],hue=i,cmap='plasma',legend=True,alpha=1.0,s=3) #

ax[ii].set_title(i)

plt.tight_layout()

plt.subplots_adjust(wspace=-0.5)

# Call function that plots two geopandas plots

plotTwo(data_cali_hp,['Population','MedInc'])

plotTwo(data_cali_hp,['HouseAge','MedHouseVal'])

#del data_cali_hp['geometry'] # not useful for anything other than gpd visualisation

C:\Users\Miguel\AppData\Local\Temp\ipykernel_22032\3254044107.py:12: UserWarning: Geometry is in a geographic CRS. Results from 'area' are likely incorrect. Use 'GeoSeries.to_crs()' to re-project geometries to a projected CRS before this operation.

cali = cali.assign(area=cali.geometry.area)

If you are not familiar with the state of California, it is interesting to notice that all datapoints show a graphical representation of this state. The high-valued houses will be located on the coast, where the big cities from California are located: San Diego, Los Angeles, San Jose, or San Francisco.

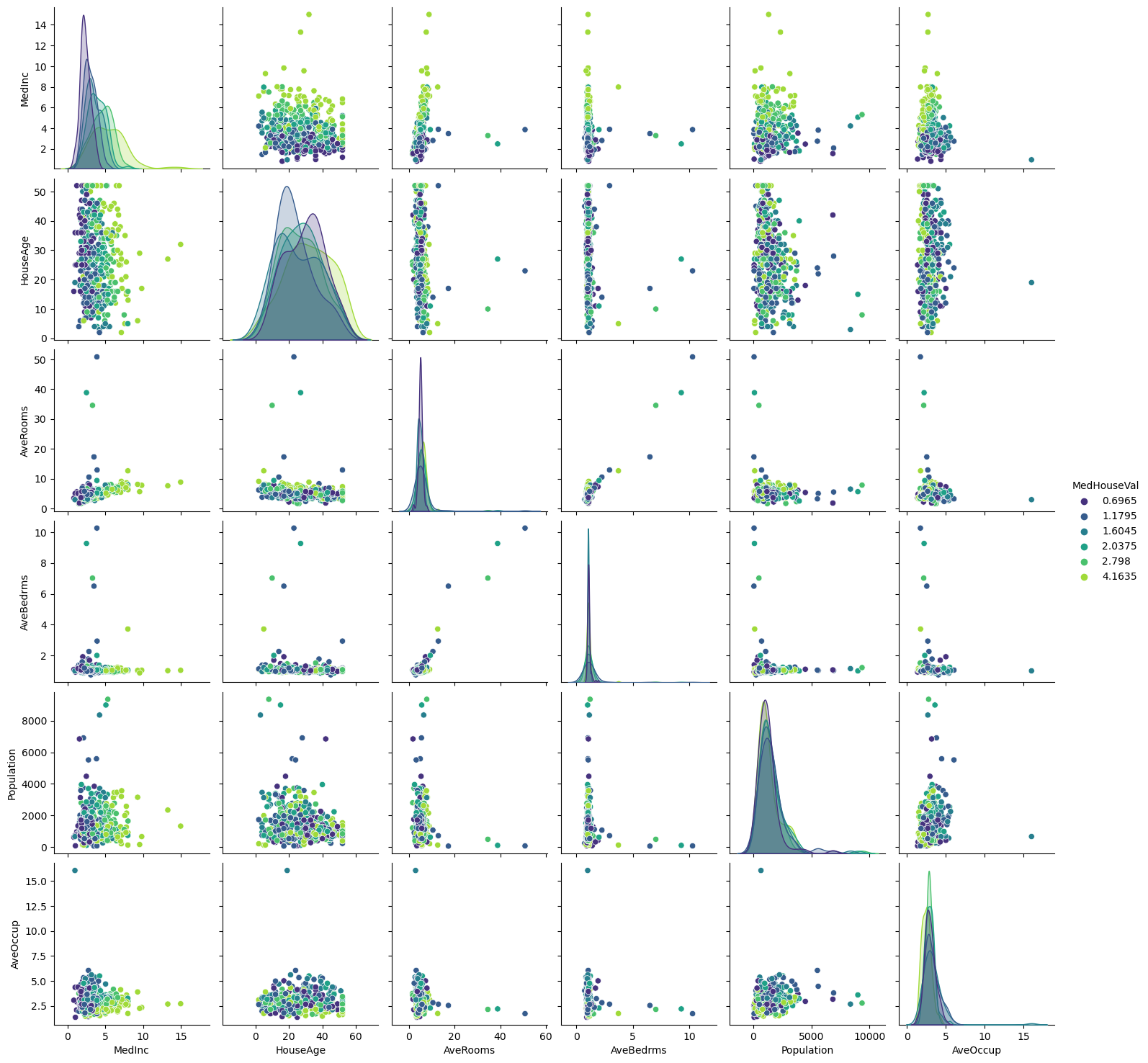

Let’s make a final analysis by making a pair plot of all features and the target but dropping the longitude and latitude. We will remove the target such that we can create proper histogram.

import pandas as pd

import numpy as np

import seaborn as sns

# Take a random sample of the data to acelerate plotting

rng = np.random.RandomState(0)

indices = rng.choice(

np.arange(data_cali_hp.shape[0]), size=500, replace=False

)

# Drop the unwanted columns

columns_drop = ["Longitude", "Latitude"]

subset = data_cali_hp.iloc[indices].drop(columns=columns_drop)

# Quantize the target and keep the midpoint for each interval

subset["MedHouseVal"] = pd.qcut(subset["MedHouseVal"], 6, retbins=False)

subset["MedHouseVal"] = subset["MedHouseVal"].apply(lambda x: x.mid)

_ = sns.pairplot(data=subset, hue="MedHouseVal", palette="viridis")

Looking at descriptive statistics helps build some intuition for the data and think about the predictive model we want to setup. We can for instance notice the presence of outliers, and see that the median income is helpful to distinguish high-valued from low-valued houses. It is reasonable to expect the longitude, latitude, and the median income to be useful features in predicting the median house values.

Predicting House Values#

Let’s setup a Bayesian Linear Regression model to try and predict house prices in Cali.

from sklearn.linear_model import BayesianRidge, LinearRegression

X = data_cali_hp.copy()

#X = (X - X.mean()) / X.std()

y = np.exp(data_cali_hp['MedHouseVal']) # <- typically we keep the log to run the regression. Here I take the exp{} so that coeffs are meaningful.

LRM = LinearRegression()

BLR = BayesianRidge()

BLR.fit(X, y)

LRM.fit(X, y)

# Create a DataFrame to store the coefficients

coefficients_df = pd.DataFrame({

'Feature': X.columns, # Assuming X contains column names

'Linear Regression Coefficient': LRM.coef_,

'Bayesian Ridge Coefficient': BLR.coef_

})

# Display the coefficients

print(coefficients_df)

Feature Linear Regression Coefficient Bayesian Ridge Coefficient

0 MedInc 1.634156 1.632060

1 HouseAge 0.175638 0.175636

2 AveRooms -2.077023 -2.069044

3 AveBedrms 8.571035 8.532918

4 Population -0.000657 -0.000657

5 AveOccup -0.001491 -0.001493

6 Latitude 8.749902 8.739650

7 Longitude 8.726341 8.716120

8 MedHouseVal 26.761079 26.753811

Note that the Bayesian Linear Regression that we described is sometimes called Bayesian Ridge due to the Gaussian Priors put on the weights \(w\). These priors penalize large values of the coefficients. For this specific data, both seem to give very similar results although this needs not be the case. Notice also that, in the above example we totally disregarded the hyperparameters \(\lambda\) and \(\sigma\). It turns out that, when using BayesianRidge() if you don’t specify their values, Python will automatically define uninformative Gamma hyperpriors. However, you can also specify hyperparameter if you have a strong opinion about what the value of a specific coefficient should be.

Exercise#

Calculate the predicted value of a house for a household with average features, using the model above.

BLR.predict([data_cali_hp.mean().values])

array([18.68512913])

Let’s write a DIY machine learning model pipeline to help us compare predictive performance.

import warnings

from sklearn.dummy import DummyRegressor

from sklearn.model_selection import cross_val_score

def suppress_warnings():

warnings.filterwarnings('ignore')

# Model Evaluation Pipeline w/ Cross Validation

def modelEval(datah,feature='MedHouseVal',model_id = 'dummy'):

# Input: Feature & Target DataFrame

# Split feature/target variable

y = datah[feature].copy()

X = datah.copy()

del X[feature] # remove target variable

suppress_warnings()

# Pick Model

if(model_id == 'dummy'): model = DummyRegressor()

if(model_id == 'BLR'): model = BayesianRidge(verbose=False) # <- set to false for minimalist output

if(model_id == 'LR'): model = LinearRegression()

''' Standard Cross Validation '''

cv_score = np.sqrt(-cross_val_score(model,X,y,cv=5,scoring='neg_mean_squared_error'))

print("RMSE:",cv_score);print("Mean across k-fold:", cv_score.mean());print("std:", cv_score.std())

# A simple comparison of models

modelEval(data_cali_hp,model_id='dummy')

modelEval(data_cali_hp,model_id='BLR')

modelEval(data_cali_hp,model_id='LR')

RMSE: [1.14300564 1.09495832 1.25408734 1.12189797 1.23064605]

Mean across k-fold: 1.1689190658050883

std: 0.06231618587595042

RMSE: [0.69598835 0.78910253 0.80387139 0.73723379 0.70327065]

Mean across k-fold: 0.7458933435919393

std: 0.04384216713047099

RMSE: [0.69631786 0.78898504 0.80387217 0.73702076 0.70333835]

Mean across k-fold: 0.7459068363518117

std: 0.04373972167592658

Exercise#

Why are the results identical for the Linear Regression and Bayesian Linear Regression ? Tweek the pipeline to allow for a much wider range of models within the linear regression model seen in previous labs. Make sure you include the Ridge, Lasso and Elastic Net. Compare the RMSE and comment.

Automatic Relevance Determination Regression#

Automatic Relevance Determination (ARD) Regression is a kind of Bayesian Linear Regression that leads to a sparser solution for \(w\).

It is best thought as a prior rather than a regression. It drops the spherical Gaussian distribution for a centered elliptic Gaussian distribution. What does that mean ? Each coefficient \(w_i\) can be independently drawn from a Gaussian distribution, centered in zero and with precision \(\lambda_i\). Thus,

with A being a positive definite diagonal matrix and \(\lambda = diag(A) = (\lambda_1,...,\lambda_d)\). Contrary to the standard Bayesian Linear Regression we introduced, here each element \(w_i\) has its own standard deviation \(1/ \lambda_i\).

Again, here \(\lambda\) is a hyperparameter which can be set by the econometrician with expert knwoledge about the DGP. However, when using ARDRegression() from sklearn, by default Gamma priors are specified. ARD is also known in the literature as Sparse Bayesian Learning and Relevance Vector Machine (see Section 7.2.1 of Chris Bishop’s Book )

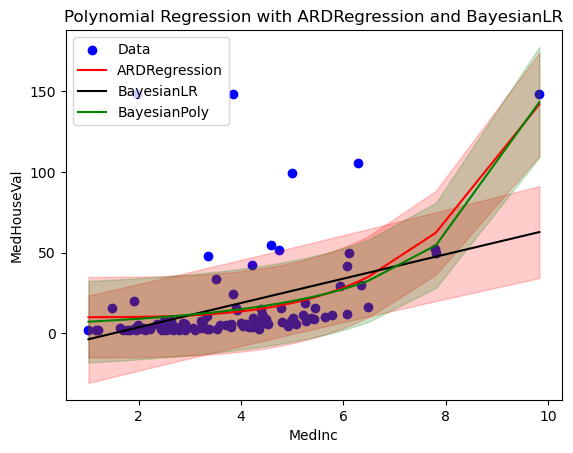

Let’s now see how the ARD Prior leads to different results with our dataset.

from sklearn.linear_model import ARDRegression

ard = ARDRegression(compute_score=True, n_iter=30).fit(X, y)

coefficients_df['ARDRegression'] = ard.coef_

coefficients_df

| Feature | Linear Regression Coefficient | Bayesian Ridge Coefficient | ARDRegression | |

|---|---|---|---|---|

| 0 | MedInc | 1.634156 | 1.632060 | 1.615543 |

| 1 | HouseAge | 0.175638 | 0.175636 | 0.194449 |

| 2 | AveRooms | -2.077023 | -2.069044 | -2.013981 |

| 3 | AveBedrms | 8.571035 | 8.532918 | 8.394052 |

| 4 | Population | -0.000657 | -0.000657 | 0.000000 |

| 5 | AveOccup | -0.001491 | -0.001493 | 0.000000 |

| 6 | Latitude | 8.749902 | 8.739650 | 8.836697 |

| 7 | Longitude | 8.726341 | 8.716120 | 8.790180 |

| 8 | MedHouseVal | 26.761079 | 26.753811 | 26.780613 |

Bayesian regressions with polynomial feature expansion#

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import PolynomialFeatures, StandardScaler

# Take a random sample of the data to acelerate plotting

rng = np.random.RandomState(0)

indices = rng.choice(

np.arange(data_cali_hp.shape[0]), size=100, replace=False

)

X = data_cali_hp[['MedInc']].iloc[indices].copy()

y = np.exp(data_cali_hp['MedHouseVal'].iloc[indices]) # <- typically we keep the log to run the regression. Here I take the exp{} so that coeffs are meaningful.

blr_poly = make_pipeline(

PolynomialFeatures(degree=1, include_bias=False),

StandardScaler(),

BayesianRidge(),

).fit(X, y)

ard_poly = make_pipeline(

PolynomialFeatures(degree=10, include_bias=False),

StandardScaler(),

ARDRegression(),

).fit(X, y)

brr_poly = make_pipeline(

PolynomialFeatures(degree=10, include_bias=False),

StandardScaler(),

BayesianRidge(),

).fit(X, y)

y_ard, y_ard_std = ard_poly.predict(X, return_std=True)

y_brr, y_brr_std = brr_poly.predict(X, return_std=True)

y_blr, y_blr_std = blr_poly.predict(X, return_std=True)

import matplotlib.pyplot as plt

# Original data points

plt.scatter(X, y, label='Data', color='b')

# Sort X for a smoother plot

X_plot = np.sort(X, axis=0)

# Predictions and standard deviations for ARDRegression

y_ard, y_ard_std = ard_poly.predict(X_plot, return_std=True)

plt.plot(X_plot, y_ard, label='ARDRegression', color='r')

plt.fill_between(X_plot[:, 0], y_ard - y_ard_std, y_ard + y_ard_std, color='r', alpha=0.2)

# Predictions and standard deviations for ARDRegression

y_blr, y_blr_std = blr_poly.predict(X_plot, return_std=True)

plt.plot(X_plot, y_blr, label='BayesianLR', color='k')

plt.fill_between(X_plot[:, 0], y_blr - y_blr_std, y_blr + y_blr_std, color='r', alpha=0.2)

# Predictions and standard deviations for BayesianRidge

y_brr, y_brr_std = brr_poly.predict(X_plot, return_std=True)

plt.plot(X_plot, y_brr, label='BayesianPoly', color='g')

plt.fill_between(X_plot[:, 0], y_brr - y_brr_std, y_brr + y_brr_std, color='g', alpha=0.2)

plt.xlabel('MedInc')

plt.ylabel('MedHouseVal')

plt.legend(loc='upper left')

plt.title('Polynomial Regression with ARDRegression and BayesianLR')

plt.show()

Exercise#

Use the make_pipeline function to construct MSE for the three models in the previous example. Which one returns the best in-sample fit ?

References#

Some good resources for further study:

Christopher M. Bishop. Pattern Recognition and Machine Learning. Springer, 2006.

Pace, R. Kelley and Ronald Barry. Sparse Spatial Autoregressions, Statistics and Probability Letters, 33 ,1997 291-297.