Decision Trees, Random Forests & Support Vector Machines#

LendingClub is a US peer-to-peer lending company that operates an online lending platform. It was founded in 2006 and is headquartered in San Francisco, California. The platform facilitates the borrowing and lending of money directly between individuals, bypassing traditional banks. Investors can construct their portfolio of loans, according to their risk appetite. Naturally, if the borrower fails to repay their loan, investors lose money. Therefore, investors face the problem of predicting the risk of a borrower being unable to repay a loan.

The firm makes loan-level data freely available online so that investors can make informed decisions about whether to invest. Let’s try and use ML models learned in class to predict whether a loan will be fully-paid or not, based on borrower characteristics. The data is available on the firms’ webpage but here we will work with a dataset available on Kaggle.

Note that the original dataset has millions of loans. To keep things simple (and avoid computational bottlenecks) we will work with a random sample of this larger dataframe. Download two excel files from Moodle ‘loan_data.xlsx’ and ‘descriptives.xlsx’ and load them to your working environment.

Load Data#

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.model_selection import train_test_split

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import classification_report,confusion_matrix

from sklearn.model_selection import RandomizedSearchCV

# Load the CSV file into a Pandas DataFrame

# Load data from the first sheet

df = pd.read_excel('loan_data.xlsx')

desc = pd.read_excel('descriptives.xlsx')

# Display the DataFrame

df.head()

---------------------------------------------------------------------------

ModuleNotFoundError Traceback (most recent call last)

File c:\Users\Miguel\anaconda3\envs\econ5129_labs\Lib\site-packages\pandas\compat\_optional.py:142, in import_optional_dependency(name, extra, errors, min_version)

141 try:

--> 142 module = importlib.import_module(name)

143 except ImportError:

File c:\Users\Miguel\anaconda3\envs\econ5129_labs\Lib\importlib\__init__.py:126, in import_module(name, package)

125 level += 1

--> 126 return _bootstrap._gcd_import(name[level:], package, level)

File <frozen importlib._bootstrap>:1204, in _gcd_import(name, package, level)

File <frozen importlib._bootstrap>:1176, in _find_and_load(name, import_)

File <frozen importlib._bootstrap>:1140, in _find_and_load_unlocked(name, import_)

ModuleNotFoundError: No module named 'openpyxl'

During handling of the above exception, another exception occurred:

ImportError Traceback (most recent call last)

Cell In[1], line 13

9 from sklearn.model_selection import RandomizedSearchCV

11 # Load the CSV file into a Pandas DataFrame

12 # Load data from the first sheet

---> 13 df = pd.read_excel('loan_data.xlsx')

14 desc = pd.read_excel('descriptives.xlsx')

16 # Display the DataFrame

File c:\Users\Miguel\anaconda3\envs\econ5129_labs\Lib\site-packages\pandas\io\excel\_base.py:478, in read_excel(io, sheet_name, header, names, index_col, usecols, dtype, engine, converters, true_values, false_values, skiprows, nrows, na_values, keep_default_na, na_filter, verbose, parse_dates, date_parser, date_format, thousands, decimal, comment, skipfooter, storage_options, dtype_backend)

476 if not isinstance(io, ExcelFile):

477 should_close = True

--> 478 io = ExcelFile(io, storage_options=storage_options, engine=engine)

479 elif engine and engine != io.engine:

480 raise ValueError(

481 "Engine should not be specified when passing "

482 "an ExcelFile - ExcelFile already has the engine set"

483 )

File c:\Users\Miguel\anaconda3\envs\econ5129_labs\Lib\site-packages\pandas\io\excel\_base.py:1513, in ExcelFile.__init__(self, path_or_buffer, engine, storage_options)

1510 self.engine = engine

1511 self.storage_options = storage_options

-> 1513 self._reader = self._engines[engine](self._io, storage_options=storage_options)

File c:\Users\Miguel\anaconda3\envs\econ5129_labs\Lib\site-packages\pandas\io\excel\_openpyxl.py:548, in OpenpyxlReader.__init__(self, filepath_or_buffer, storage_options)

533 @doc(storage_options=_shared_docs["storage_options"])

534 def __init__(

535 self,

536 filepath_or_buffer: FilePath | ReadBuffer[bytes],

537 storage_options: StorageOptions = None,

538 ) -> None:

539 """

540 Reader using openpyxl engine.

541

(...)

546 {storage_options}

547 """

--> 548 import_optional_dependency("openpyxl")

549 super().__init__(filepath_or_buffer, storage_options=storage_options)

File c:\Users\Miguel\anaconda3\envs\econ5129_labs\Lib\site-packages\pandas\compat\_optional.py:145, in import_optional_dependency(name, extra, errors, min_version)

143 except ImportError:

144 if errors == "raise":

--> 145 raise ImportError(msg)

146 return None

148 # Handle submodules: if we have submodule, grab parent module from sys.modules

ImportError: Missing optional dependency 'openpyxl'. Use pip or conda to install openpyxl.

# print descriptives of the variables

desc

| credit.policy | if the customer meets the credit underwriting criteria of LendingClub.com, and 0 otherwise. | |

|---|---|---|

| 0 | purpose | The purpose of the loan (takes values "credit_... |

| 1 | int.rate | The purpose of the loan (takes values "credit_... |

| 2 | installment | The purpose of the loan (takes values "credit_... |

| 3 | log.annual.inc | The natural log of the self-reported annual in... |

| 4 | dti | The debt-to-income ratio of the borrower (amou... |

| 5 | fico | The FICO credit score of the borrower. |

| 6 | days.with.cr.line | The number of days the borrower has had a cred... |

| 7 | revol.bal | The borrower's revolving balance (amount unpai... |

| 8 | revol.util | The borrower's revolving balance (amount unpai... |

| 9 | inq.last.6mths | The borrower's number of inquiries by creditor... |

| 10 | delinq.2yrs | The number of times the borrower had been 30+ ... |

| 11 | pub.rec | The borrower's number of derogatory public rec... |

| 12 | not.fully.paid | not fully paid. |

Data Descriptives#

To have a feel for the data it’s always a good idea to start with simple descriptive statistics. Because our focus is on classification (ie. predict delinquencies), let’s also plot some descriptives for loans that have and have not been fully paid.

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 9578 entries, 0 to 9577

Data columns (total 14 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 credit.policy 9578 non-null int64

1 purpose 9578 non-null object

2 int.rate 9578 non-null float64

3 installment 9578 non-null float64

4 log.annual.inc 9578 non-null float64

5 dti 9578 non-null float64

6 fico 9578 non-null int64

7 days.with.cr.line 9578 non-null float64

8 revol.bal 9578 non-null int64

9 revol.util 9578 non-null float64

10 inq.last.6mths 9578 non-null int64

11 delinq.2yrs 9578 non-null int64

12 pub.rec 9578 non-null int64

13 not.fully.paid 9578 non-null int64

dtypes: float64(6), int64(7), object(1)

memory usage: 1.0+ MB

df.describe().round(2)

| credit.policy | int.rate | installment | log.annual.inc | dti | fico | days.with.cr.line | revol.bal | revol.util | inq.last.6mths | delinq.2yrs | pub.rec | not.fully.paid | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 9578.0 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 | 9578.00 |

| mean | 0.8 | 0.12 | 319.09 | 10.93 | 12.61 | 710.85 | 4560.77 | 16913.96 | 46.80 | 1.58 | 0.16 | 0.06 | 0.16 |

| std | 0.4 | 0.03 | 207.07 | 0.61 | 6.88 | 37.97 | 2496.93 | 33756.19 | 29.01 | 2.20 | 0.55 | 0.26 | 0.37 |

| min | 0.0 | 0.06 | 15.67 | 7.55 | 0.00 | 612.00 | 178.96 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| 25% | 1.0 | 0.10 | 163.77 | 10.56 | 7.21 | 682.00 | 2820.00 | 3187.00 | 22.60 | 0.00 | 0.00 | 0.00 | 0.00 |

| 50% | 1.0 | 0.12 | 268.95 | 10.93 | 12.66 | 707.00 | 4139.96 | 8596.00 | 46.30 | 1.00 | 0.00 | 0.00 | 0.00 |

| 75% | 1.0 | 0.14 | 432.76 | 11.29 | 17.95 | 737.00 | 5730.00 | 18249.50 | 70.90 | 2.00 | 0.00 | 0.00 | 0.00 |

| max | 1.0 | 0.22 | 940.14 | 14.53 | 29.96 | 827.00 | 17639.96 | 1207359.00 | 119.00 | 33.00 | 13.00 | 5.00 | 1.00 |

Visualization#

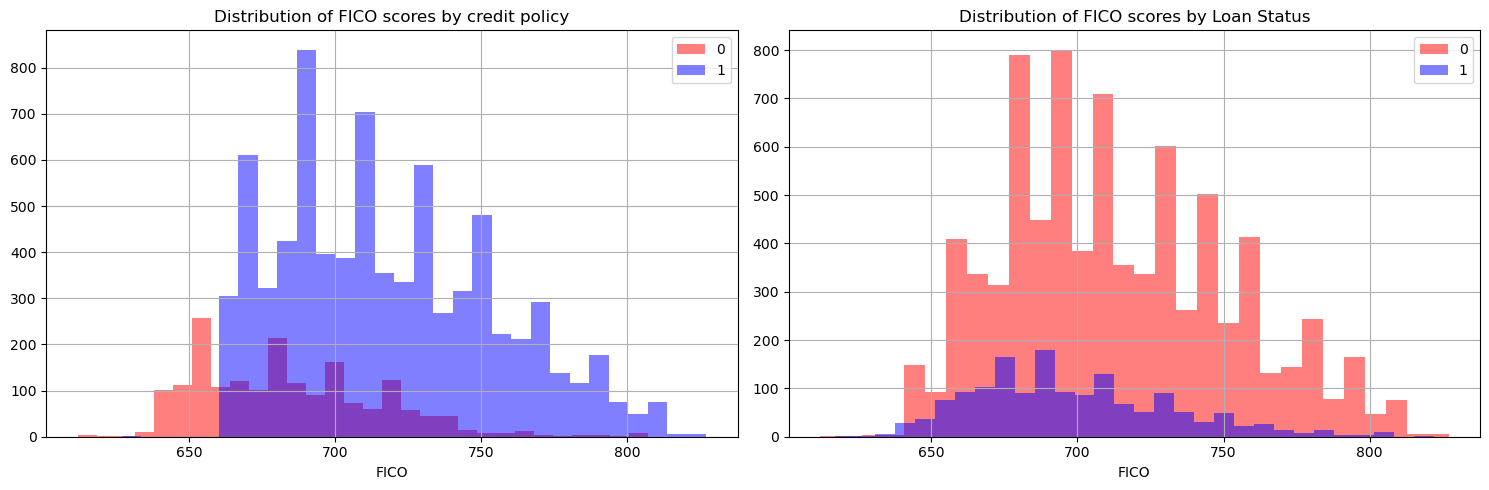

FICO scores ought to be an important variable for loan delinquency prediction as they measure borrower quality. To understand the firms’ credit policy with respect to FICO scores and how FICO scores differ across borrowers, let’s plot a histogram of borrowers that comply with Lending Club’s credit policy and have fully repaid their loss.

# Set up subplots with 1 row and 2 columns

plt.figure(figsize=(15, 5))

# Common color for both histograms

color = 'blue'

# Plot the first histogram

plt.subplot(1, 2, 1)

df[df['credit.policy']==0]['fico'].hist(bins=30, alpha=0.5, label='0', color='red')

df[df['credit.policy']==1]['fico'].hist(bins=30, alpha=0.5, label='1', color=color)

plt.legend()

plt.xlabel('FICO')

plt.title('Distribution of FICO scores by credit policy')

# Plot the first histogram

plt.subplot(1, 2, 2)

df[df['not.fully.paid']==0]['fico'].hist(bins=30, alpha=0.5, label='0', color='red')

df[df['not.fully.paid']==1]['fico'].hist(bins=30, alpha=0.5, label='1', color=color)

plt.legend()

plt.xlabel('FICO')

plt.title('Distribution of FICO scores by Loan Status')

# Adjust layout for better spacing

plt.tight_layout()

# Show the plot

plt.show()

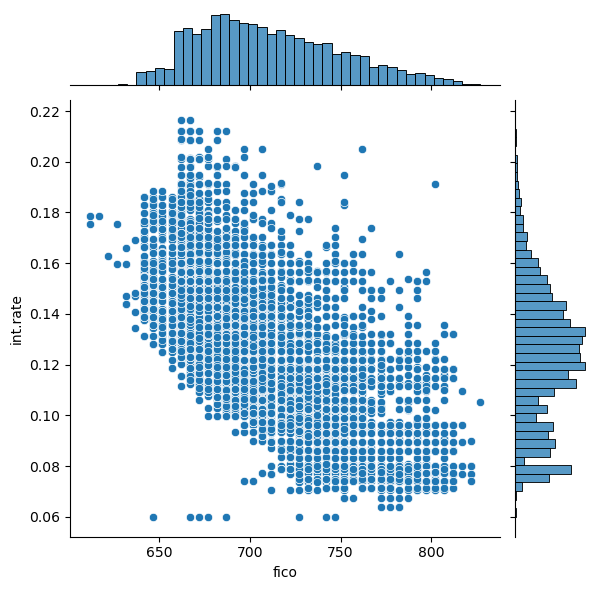

Now, let’s also have a look at the distribution of FICO scores, interest rates charged and how they relate to each other.

sns.jointplot(x='fico',y='int.rate',data=df)

<seaborn.axisgrid.JointGrid at 0x288650b0d50>

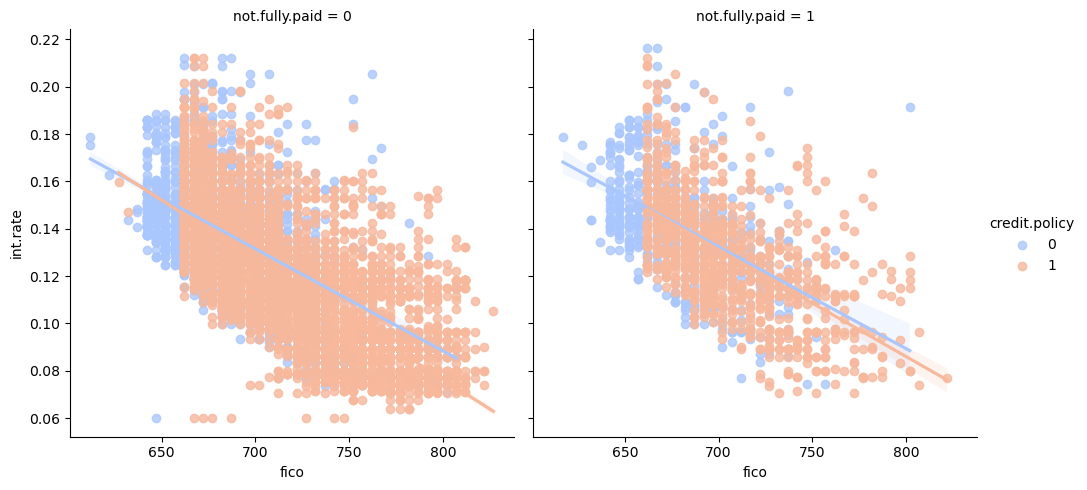

sns.lmplot(x='fico',y='int.rate',data=df,col='not.fully.paid',hue='credit.policy',palette='coolwarm')

<seaborn.axisgrid.FacetGrid at 0x288653b3210>

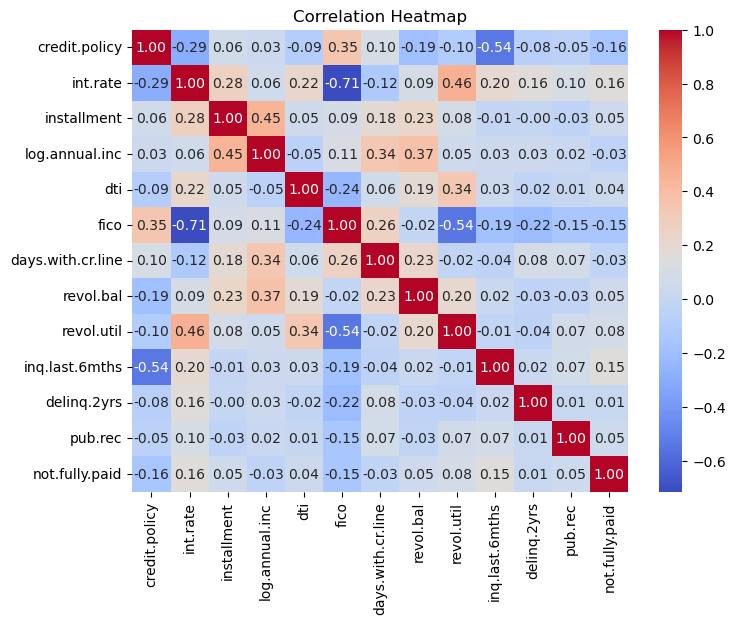

Given a FICO score, there seems to be greater dispersion, in terms of interest rates charges, of borrowers that haven’t paid their loan back fully and therefore may default. This is a reminder that other variables should also be taken into account when considering delinquency likelihoods. Before we start processing the data and building our ML model, let’s look at the correlation amongst the variables.

# Select numerical columns from your DataFrame

numerical_columns = df.select_dtypes(include=['number'])

# Create a heatmap of the correlation matrix

plt.figure(figsize=(8, 6))

sns.heatmap(numerical_columns.corr(), annot=True, cmap='coolwarm', fmt=".2f")

plt.title('Correlation Heatmap')

plt.show()

Now convert some categorical variables into dummy variables so that they can be added to the feature set of our ML model.

df = pd.get_dummies(df,columns=['purpose'],drop_first=True)

df

| credit.policy | int.rate | installment | log.annual.inc | dti | fico | days.with.cr.line | revol.bal | revol.util | inq.last.6mths | delinq.2yrs | pub.rec | not.fully.paid | purpose_credit_card | purpose_debt_consolidation | purpose_educational | purpose_home_improvement | purpose_major_purchase | purpose_small_business | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0.1189 | 829.10 | 11.350407 | 19.48 | 737 | 5639.958333 | 28854 | 52.1 | 0 | 0 | 0 | 0 | False | True | False | False | False | False |

| 1 | 1 | 0.1071 | 228.22 | 11.082143 | 14.29 | 707 | 2760.000000 | 33623 | 76.7 | 0 | 0 | 0 | 0 | True | False | False | False | False | False |

| 2 | 1 | 0.1357 | 366.86 | 10.373491 | 11.63 | 682 | 4710.000000 | 3511 | 25.6 | 1 | 0 | 0 | 0 | False | True | False | False | False | False |

| 3 | 1 | 0.1008 | 162.34 | 11.350407 | 8.10 | 712 | 2699.958333 | 33667 | 73.2 | 1 | 0 | 0 | 0 | False | True | False | False | False | False |

| 4 | 1 | 0.1426 | 102.92 | 11.299732 | 14.97 | 667 | 4066.000000 | 4740 | 39.5 | 0 | 1 | 0 | 0 | True | False | False | False | False | False |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 9573 | 0 | 0.1461 | 344.76 | 12.180755 | 10.39 | 672 | 10474.000000 | 215372 | 82.1 | 2 | 0 | 0 | 1 | False | False | False | False | False | False |

| 9574 | 0 | 0.1253 | 257.70 | 11.141862 | 0.21 | 722 | 4380.000000 | 184 | 1.1 | 5 | 0 | 0 | 1 | False | False | False | False | False | False |

| 9575 | 0 | 0.1071 | 97.81 | 10.596635 | 13.09 | 687 | 3450.041667 | 10036 | 82.9 | 8 | 0 | 0 | 1 | False | True | False | False | False | False |

| 9576 | 0 | 0.1600 | 351.58 | 10.819778 | 19.18 | 692 | 1800.000000 | 0 | 3.2 | 5 | 0 | 0 | 1 | False | False | False | True | False | False |

| 9577 | 0 | 0.1392 | 853.43 | 11.264464 | 16.28 | 732 | 4740.000000 | 37879 | 57.0 | 6 | 0 | 0 | 1 | False | True | False | False | False | False |

9578 rows × 19 columns

segregate features from the output which in this case is ‘not.fully.paid’.

X=df.drop('not.fully.paid', axis=1)

y=df['not.fully.paid']

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.30)

Decision Trees#

Decision Trees are a popular machine learning model used for both classification and regression tasks (though here we use it for classification solely). Here is a brief summary of the intuition behind Decision Trees:

Structure:

Hierarchical Structure: Decision Trees organize data in a hierarchical manner.

Nodes: Internal nodes represent decisions based on specific features.

Decision Making:

Traversal: The model makes decisions by traversing the tree from the root to a leaf.

Feature-based Decisions: At each internal node, a decision is made based on a specific feature, leading to a branch.

Splitting Criteria:

Objective: The tree learns to split the data by selecting features and thresholds that maximize information gain.

Types:

Classification Trees: Leaf nodes represent different classes, and the majority class is assigned to instances in a leaf.

Regression Trees: Leaf nodes represent numeric values, usually the mean of the target values of instances in that leaf.

Pruning:

Overfitting: To prevent overfitting, trees can be pruned by removing branches that do not significantly contribute to predictive performance.

Ensemble Methods:

Random Forests and Gradient Boosted Trees: Decision Trees are often used as building blocks in ensemble methods to improve predictive accuracy and robustness.

Interpretability:

Visual Decision Process: Decision Trees offer interpretability, making it easy to understand the decision-making process and communicate.

Remarks:

Sensitive to Data Distribution: Decision Trees can be sensitive to variations in the training data, leading to different tree structures for slightly different datasets.

Handling Missing Values: Some implementations can handle missing values during the learning process.

Decision Trees provide a flexible and interpretable approach to machine learning, with the potential for overfitting mitigated through pruning and ensemble methods. Let’s use Decision trees to help predict whether a loan is fully paid or not.

dtree = DecisionTreeClassifier()

dtree.fit(X_train,y_train)

pred = dtree.predict(X_test)

print(classification_report(y_test,pred))

print(confusion_matrix(y_test,pred))

precision recall f1-score support

0 0.85 0.84 0.85 2422

1 0.21 0.23 0.22 452

accuracy 0.74 2874

macro avg 0.53 0.54 0.53 2874

weighted avg 0.75 0.74 0.75 2874

[[2030 392]

[ 346 106]]

Random forest is a popular supervised machine learning method for classification and regression that consists of using several decision trees, and combining the trees’ predictions into an overall prediction. To train the random forest is to train each of its decision trees independently. Each decision tree is typically trained on a slightly different part of the training set, and may look at different features for its node splits. Let’s also fit a Random Forest to our data.

rf = RandomForestClassifier()

rf.fit(X_train,y_train)

pred1=rf.predict(X_test)

print(classification_report(y_test,pred1))

print(confusion_matrix(y_test,pred1))

precision recall f1-score support

0 0.85 0.99 0.91 2422

1 0.44 0.03 0.05 452

accuracy 0.84 2874

macro avg 0.64 0.51 0.48 2874

weighted avg 0.78 0.84 0.78 2874

[[2407 15]

[ 440 12]]

As you see Random Forests take longer to run (even though our dataset is small). They deliver slightly better performance statistics.

Exercise#

Tune our random forest by using ‘RandomizedSearchCV()’ function in sklearn and comment on prediction gains.

n_estimators = [int(x) for x in np.linspace(start = 200, stop = 1000, num = 5)]

max_features = ['auto', 'sqrt']

max_depth = [int(x) for x in np.linspace(20, 100, num = 5)]

max_depth.append(None)

min_samples_split = [2, 5, 10]

min_samples_leaf = [1, 2, 4]

bootstrap = [True, False]

random_grid = {'n_estimators': n_estimators,

'max_features': max_features,

'max_depth': max_depth,

'min_samples_split': min_samples_split,

'min_samples_leaf': min_samples_leaf,

'bootstrap': bootstrap}

rf1 = RandomForestClassifier()

rf2 = RandomizedSearchCV(estimator = rf1, param_distributions = random_grid,

cv = 3, verbose=2,n_jobs = -1)

rf2.fit(X_train,y_train)

Fitting 3 folds for each of 10 candidates, totalling 30 fits

RandomizedSearchCV(cv=3, estimator=RandomForestClassifier(), n_jobs=-1,

param_distributions={'bootstrap': [True, False],

'max_depth': [20, 40, 60, 80, 100,

None],

'max_features': ['auto', 'sqrt'],

'min_samples_leaf': [1, 2, 4],

'min_samples_split': [2, 5, 10],

'n_estimators': [200, 400, 600, 800,

1000]},

verbose=2)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

RandomizedSearchCV(cv=3, estimator=RandomForestClassifier(), n_jobs=-1,

param_distributions={'bootstrap': [True, False],

'max_depth': [20, 40, 60, 80, 100,

None],

'max_features': ['auto', 'sqrt'],

'min_samples_leaf': [1, 2, 4],

'min_samples_split': [2, 5, 10],

'n_estimators': [200, 400, 600, 800,

1000]},

verbose=2)RandomForestClassifier()

RandomForestClassifier()

rf2.best_params_

{'n_estimators': 800,

'min_samples_split': 5,

'min_samples_leaf': 4,

'max_features': 'sqrt',

'max_depth': 60,

'bootstrap': True}

rf3=RandomForestClassifier(n_estimators= 200,

min_samples_split=2,

min_samples_leaf=2,

max_features='auto',

max_depth=40,

bootstrap=True)

rf3.fit(X_train,y_train)

preds3=rf3.predict(X_test)

print(classification_report(y_test,preds3))

print(confusion_matrix(y_test,preds3))

c:\Users\Miguel\anaconda3\Lib\site-packages\sklearn\ensemble\_forest.py:424: FutureWarning: `max_features='auto'` has been deprecated in 1.1 and will be removed in 1.3. To keep the past behaviour, explicitly set `max_features='sqrt'` or remove this parameter as it is also the default value for RandomForestClassifiers and ExtraTreesClassifiers.

warn(

precision recall f1-score support

0 0.84 1.00 0.91 2422

1 0.36 0.01 0.02 452

accuracy 0.84 2874

macro avg 0.60 0.50 0.47 2874

weighted avg 0.77 0.84 0.77 2874

[[2413 9]

[ 447 5]]

Support Vector Machines (SVMs)#

SVMs are Supervised learning algorithms for classification and regression. They work by finding a hyperplane that best separates data points into different classes while maximizing the margin. Remember that a hyperplane is a decision boundary that separates data points of different classes. The margin is the distance between the hyperplane and the nearest data point from either class. SVMs seek to maximize this margin, promoting better generalization to new, unseen data.

Support Vectors:#

Definition: Support vectors are the data points that lie closest to the hyperplane and influence its position.

SVMs are named after these crucial data points as they support the definition of the decision boundary.

Types:#

1. Linear SVM:#

Hyperplane: A straight line in 2D, a plane in 3D, and a hyperplane in higher dimensions.

Use Case: Suitable for linearly separable data.

2. Non-Linear SVM (Kernel Trick):#

Idea: Transform data into a higher-dimensional space to make it linearly separable.

Kernel Functions: Radial Basis Function (RBF), Polynomial, Sigmoid, etc., are used to achieve non-linear separations.

The advantages of support vector machines are:#

Effective in high dimensional spaces.

Still effective in cases where number of dimensions is greater than the number of samples.

Uses a subset of training points in the decision function (called support vectors), so it is also memory efficient.

Versatile: different Kernel functions can be specified for the decision function. Common kernels are provided, but it is also possible to specify custom kernels.

The disadvantages of support vector machines include:#

If the number of features is much greater than the number of samples, avoid over-fitting in choosing Kernel functions and regularization term is crucial.

SVMs do not directly provide probability estimates, these are calculated using an expensive five-fold cross-validation (see Scores and probabilities, below).

Commonly used for:#

Image Classification, Text Classification, and Bioinformatics.

Tips:#

Normalize Features: It is often beneficial to normalize input features to ensure equal importance in the model.

Support Vector Machines are powerful and versatile classifiers, effective in scenarios with complex decision boundaries and high-dimensional feature spaces. Let’s explore their performance with our loan data.

# Import Support Vector Machine classifier

from sklearn.svm import SVC

# Create a Support Vector Machine classifier

svm_classifier = SVC()

# Train the Support Vector Machine classifier on the training data

svm_classifier.fit(X_train, y_train)

# Make predictions on the test data

svm_pred = svm_classifier.predict(X_test)

# Print the classification report for SVM

print("Support Vector Machine - Classification Report:\n", classification_report(y_test, svm_pred))

# Print the confusion matrix for SVM

print("Support Vector Machine - Confusion Matrix:\n", confusion_matrix(y_test, svm_pred))

Support Vector Machine - Classification Report:

precision recall f1-score support

0 0.84 1.00 0.91 2422

1 0.33 0.00 0.00 452

accuracy 0.84 2874

macro avg 0.59 0.50 0.46 2874

weighted avg 0.76 0.84 0.77 2874

Support Vector Machine - Confusion Matrix:

[[2420 2]

[ 451 1]]

Exercise#

Similarly to what you did with Random Forests, Tune the SVM for loan classification.

from sklearn.model_selection import RandomizedSearchCV, train_test_split

from sklearn.svm import LinearSVC

from sklearn.preprocessing import StandardScaler

from sklearn.metrics import classification_report, confusion_matrix

from scipy.stats import uniform

import numpy as np

# Assuming you have already loaded your data into X and y

# Split the data into training and test sets

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.30)

# Create a StandardScaler object

scaler = StandardScaler()

# Fit and transform training data

X_train_standardized = scaler.fit_transform(X_train)

# Transform test data using the same scaler

X_test_standardized = scaler.transform(X_test)

# Define a more compact parameter distribution for random search

param_dist = {

'C': uniform(0.1, 1), # Uniform distribution between 0.1 and 1

'penalty': ['l1', 'l2'], # Penalty term for LinearSVC

'dual': [False], # Dual parameter for LinearSVC

}

# Create a Linear Support Vector Machine classifier

linear_svm_classifier = LinearSVC()

# Use RandomizedSearchCV for a more efficient search

random_search = RandomizedSearchCV(linear_svm_classifier, param_dist, n_iter=20, cv=3, scoring='accuracy', verbose=1, n_jobs=-1)

random_search.fit(X_train_standardized, y_train)

# Get the best hyperparameters

best_params_random = random_search.best_params_

print("Best Hyperparameters (Random Search):", best_params_random)

# Make predictions on the test data using the best model from random search

best_linear_svm_random = random_search.best_estimator_

linear_svm_pred_random = best_linear_svm_random.predict(X_test_standardized)

# Evaluate the performance of the tuned Linear SVM

print("Tuned Linear Support Vector Machine (Random Search) - Classification Report:\n", classification_report(y_test, linear_svm_pred_random))

print("Tuned Linear Support Vector Machine (Random Search) - Confusion Matrix:\n", confusion_matrix(y_test, linear_svm_pred_random))

Fitting 3 folds for each of 20 candidates, totalling 60 fits

Best Hyperparameters (Random Search): {'C': 1.0872834785177143, 'dual': False, 'penalty': 'l1'}

Tuned Linear Support Vector Machine (Random Search) - Classification Report:

precision recall f1-score support

0 0.83 1.00 0.91 2393

1 0.00 0.00 0.00 481

accuracy 0.83 2874

macro avg 0.42 0.50 0.45 2874

weighted avg 0.69 0.83 0.76 2874

Tuned Linear Support Vector Machine (Random Search) - Confusion Matrix:

[[2389 4]

[ 481 0]]

Some notes about the exercise:

Performing grid-search with a SVM with a nonlinear Kernel is a computationally prohibitive task.

Kernelized SVMs require the computation of a distance function between each point in the dataset, which is the dominating cost of \(O(n_{features},n^2_{observations})\).

To make this task feasible, it helps to think about it a bit before writing code:

Standardizing the features helps a lot because the Kernel requires the storage of the distances putting a burden on memory

Using

RandomizedSearchCV()instead ofGridSearchCV()also helps.Another option is to use

LinearSVC().